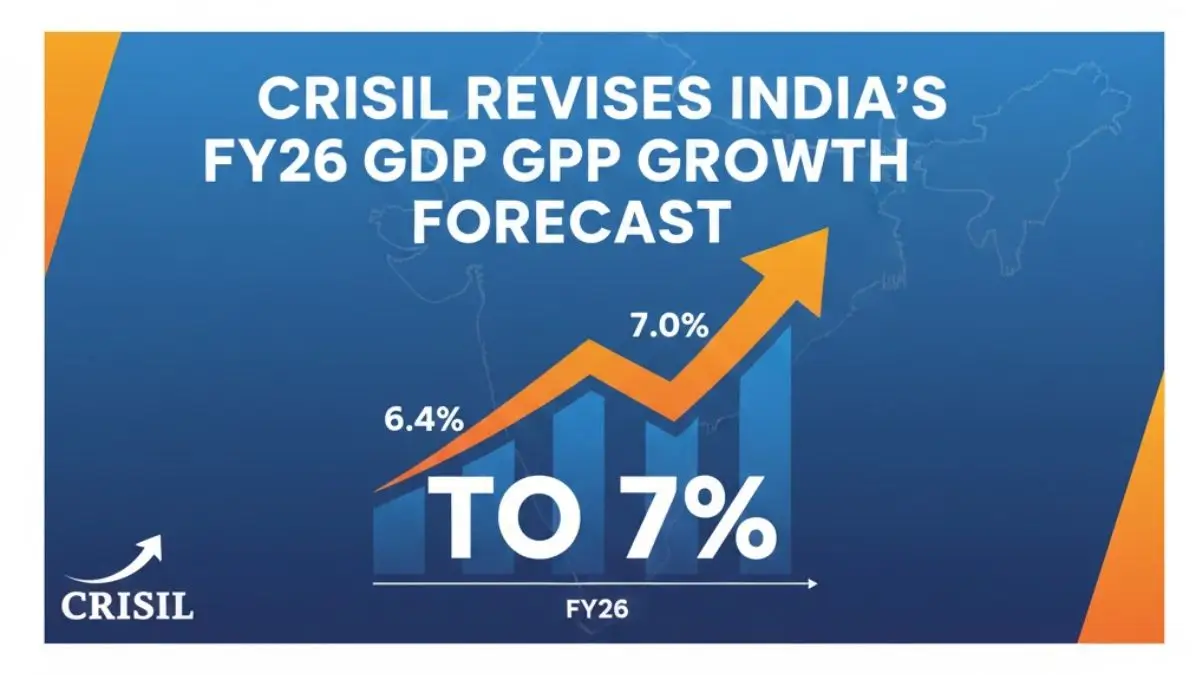

Crisil has revised its GDP growth forecast for India for the current financial year (FY26) to 7%, up from its earlier estimate of 6.5%, following an unexpectedly strong economic performance in the first half of the year. This revision reflects India’s resilient domestic demand, robust private consumption, and strong output in manufacturing and services.

The upward revision follows official data showing India’s real GDP grew by 8.2% in the second quarter (July–September) and 8% over the first half (April–September) of FY26.

Key Highlights of Crisil’s GDP Forecast

- Revised FY26 GDP Forecast: 7% (previously 6.5%)

- Q2 FY26 Real GDP Growth: 8.2%

- Nominal GDP Growth in Q2: 8.7%, moderated due to easing inflation

- Projected H2 FY26 Growth: 6.1%, due to external headwinds

Drivers of the Upward Revision

1. Strong Private Consumption

Crisil attributes the high growth to a surge in private consumption, driven by,

- Lower food inflation, which freed up disposable income

- GST rate rationalisation, making goods and services more affordable

- Reduced income tax burden and supportive interest rate environment

This uptick in consumption was particularly evident in urban discretionary spending during the festive season, boosting sectors like retail, hospitality, and transportation.

2. Manufacturing and Services Growth

From the supply side, manufacturing and services recorded significant growth, benefiting from,

- Recovery in exports despite global volatility

- Supply chain normalisation

- Increased demand in IT, financial, and business services

3. Policy Support

The economic momentum has also been aided by,

- Monetary policy easing, with the RBI’s repo rate cuts helping revive credit demand

- Public capital expenditure, especially in infrastructure and transport sectors

- Stabilising oil prices, which reduced the import bill and inflationary pressure

Outlook for Second Half of FY26

Despite the strong H1 performance, Crisil expects a moderation in growth to around 6.1% in H2, citing,

- Global headwinds, including higher US tariffs and slowdown in global trade

- Stabilisation of government spending, with capital expenditure expected to flatten

- Delayed recovery in private investment, although a mild uptick is possible

Nonetheless, Crisil maintains that fiscal and monetary policies, coupled with strong consumption patterns, will cushion the impact of external pressures.

RBI MPC Meeting 2026, Kept Repo Rates Un...

RBI MPC Meeting 2026, Kept Repo Rates Un...

India's Major Ports Handle Record 915.17...

India's Major Ports Handle Record 915.17...

Moody's Cuts India's FY27 Growth Forecas...

Moody's Cuts India's FY27 Growth Forecas...