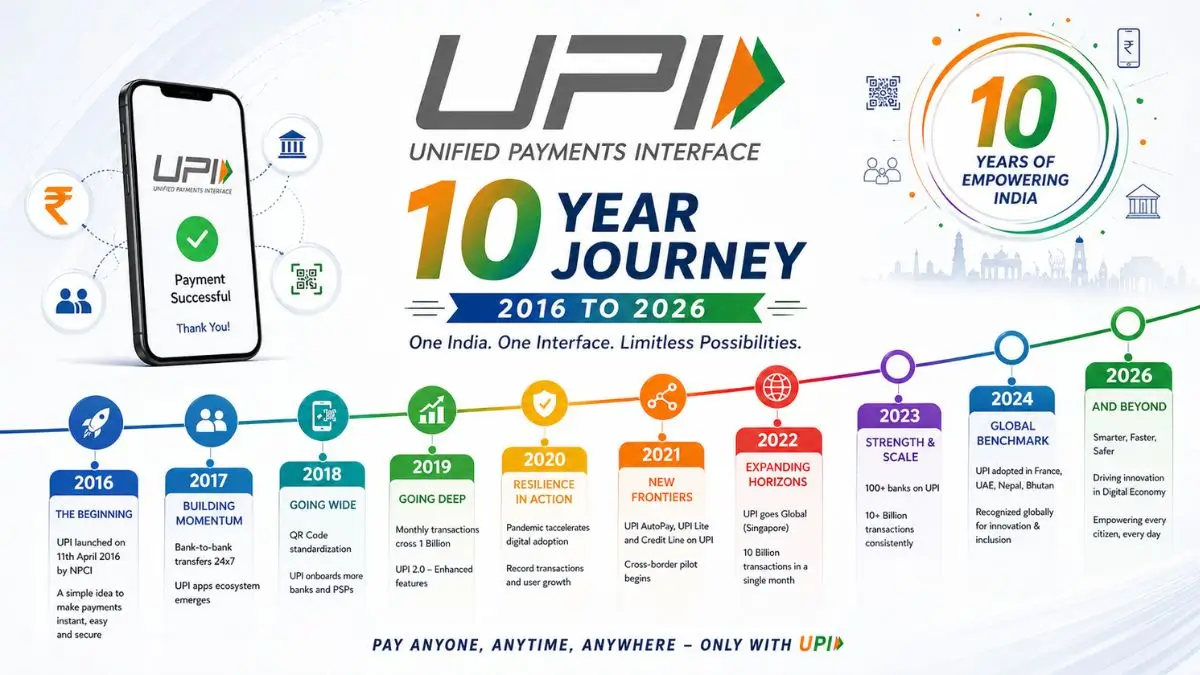

India’s Unified Payments Interface (UPI) has completed the remarkable decade after its launch on 11th April 2016 by the National Payments Corporation of India (NPCI) under the supervision of the Reserve Bank of India (RBI). Over these ten years the UPI have transformed from the modest payment platform into the world’s largest real-time payments system and processing the massive daily transactions and becoming the backbone of the country’s digital economy.

The Decade of Unmatched Growth and Scale

The journey of UPI reflects the exponential growth in both transaction volume and value and it is showcasing the widespread adoption across the urban and rural India.

From just 2 crore transactions in the FY 2016-17 the UPI have surged to over 24,162 crore transactions in the FY 2025-26 and it is marking the 12,000-fold increase.

Similarly the total transaction value have skyrocketed from the ₹0.07 lakh crore to approx. around the ₹314 lakh crore which is over a the 4,000-fold rise.

This growth have highlights how the UPI has become the integral part of daily life and enables the seamless payments from the street vendors to the large businesses.

Key Statistics Which Have Define UPI’s Success

The scale of the UPI to be understand through the latest performance indicators:

- Annual Transactions (FY 2025-26): 24,161.69 crore

- Annual Value: ₹314 lakh crore

- Daily Average Transactions: 66 crore

- Monthly Peak (March 2026): 2,264 crore transactions

- Banks on UPI: 703 (up from 21 at launch)

- Share in the India’s Digital Payments: 85%

- Global Share of in Real-Time Payments: 49%

These numbers have underline the UPI’s dominance not just only in India but also the worldwide.

Why UPI Became the Backbone of Digital Payments

The success of the UPI lies in the unique design and accessibility. It will allows users to transfer the money instantly by using mobile apps without needing bank details repeatedly.

Several factors have contributed to the its rapid adoption.

Interoperability

In which it works across the all banks and apps.

Instant Settlement

Providing the real-time fund transfer 24/7 and 365 days.

Zero or Low Cost

The process is affordable for the users and merchants.

Ease of Use

It is the simple mobile-based interface to use efficiently.

Government Push

The backing of the strong policy and digital infrastructure support from the government.

This combination have made the UPI the preferred choice for the high-frequency retail payments.

P2P vs P2M: Understanding UPI Usage Trends

UPI transactions can be divided broadly into two categories.

Person-to-Merchant (P2M)

It accounts for the 63% of transaction volume and mainly driven by small-value payments like groceries, transport and daily purchases.

Notably the 86% of these transactions are below ₹500 and it is highlighting the UPI’s role in micro-payments.

Person-to-Person (P2P)

It contributes around the 71% of transaction value which is indicating the its use in the higher-value transfers such as rent, personal payments and business dealings.

This dual nature of the UPI makes efficient for the both mass retail tool and a trusted transfer system.

UPI Goes Global and Digital Model for World

Also the UPI is no longer just limited to India but it is rapidly expanding across the borders. It has been recognized by the International Monetary Fund (IMF) as the largest real-time payment system in the world and UPI now accounts for nearly the 49% of global real-time transaction volume.

Countries where UPI is operational includes the,

- UAE

- Singapore (linked with PayNow)

- France

- Bhutan

- Nepal

- Sri Lanka

- Mauritius

- Qatar

This expansion of UPI supports the Indian travelers and diaspora while positioning the India as a leader in digital public infrastructure.

What is UPI and Why It Matters

The Unified Payments Interface (UPI) is the real-time payment system which enables the instant money transfer between the bank accounts using mobile devices.

It also has ability to handle real-time transactions, integrate multiple bank accounts and offer the versatile payment methods has revolutionized the way people conduct financial transactions.

Users can transfer money to any bank account 24/7 by ensuring the seamless and fast payments at any time.

Also the users can access multiple bank accounts through a single app it eliminates the need for multiple banking applications.

Question

Q. UPI is currently live in how many countries (approx.)?

A. 5

B. 8+

C. 10

D. 15

President Murmu Unveils Mahatma Gandhi B...

President Murmu Unveils Mahatma Gandhi B...

India Achieves 99.6% Railway Electrifica...

India Achieves 99.6% Railway Electrifica...

Killai Becomes Tamil Nadu's First Climat...

Killai Becomes Tamil Nadu's First Climat...